Learn how marketplaces like Reverb drive retention and cost savings here!

Learn how marketplaces like Reverb drive retention and cost savings here!

—

Learn MoreLearn More.svg)

September 25, 2025

Marketplaces have become the backbone of modern commerce, connecting buyers and sellers across every category—from handmade crafts to enterprise procurement. But behind the scenes, marketplace operators face a unique set of challenges: paying sellers efficiently, keeping buyers engaged, and managing the costs of payments at scale.

In this post, we’ll walk through the different types of marketplaces and highlight common use cases that operators need to solve—from payouts to refunds to loyalty. We’ll also show how Ansa helps marketplaces streamline payments, lower transaction costs, and unlock new ways to drive retention with stored value wallets and incentives.

From your local farmer to the largest retail platforms on earth, marketplaces are increasingly the way consumers find the goods they want, and merchants find the consumers they need. Let’s take a minute to talk about the types of marketplaces this blog will be useful for:

Have an additional use case in mind? We love to solution with folks! Just share your information in this form and one of our specialists will reach out.

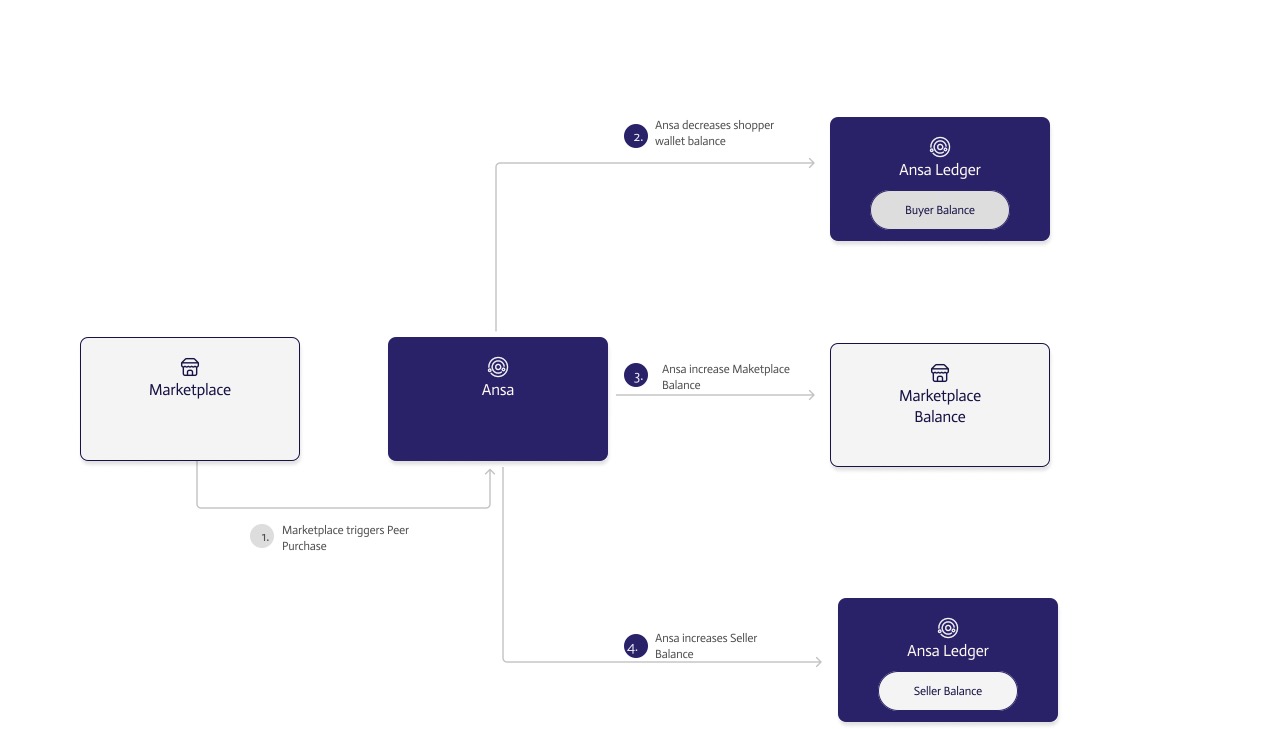

So, how does it work? When a purchase is made, the marketplace sends the details of that purchase to the Ansa platform via API. Ansa decreases the buyer’s balance, increases the seller’s balance, and sets aside the marketplace’s share—all in a single API call. These flows can happen synchronously, or after your risk team clears the transaction.

Your customers only see their spendable balance, but under the hood, a lot is happening: funding sources, incentive rules, and settlement logic all drive that simple wallet balance.

Additionally, we've built in the flexibility to work with your system.

Whether you’re building a peer-to-peer community, scaling a B2B platform, or selling digital goods, the way money moves on your marketplace has a direct impact on growth. With Ansa, you can simplify complex payment flows, reduce costs, and turn transactions into opportunities to keep buyers and sellers engaged.

If you’re ready to explore how a stored value wallet and incentive engine can work for your marketplace, our team would love to show you what’s possible.

Marketplaces have become the backbone of modern commerce, connecting buyers and sellers across every category—from handmade crafts to enterprise procurement. But behind the scenes, marketplace operators face a unique set of challenges: paying sellers efficiently, keeping buyers engaged, and managing the costs of payments at scale.

In this post, we’ll walk through the different types of marketplaces and highlight common use cases that operators need to solve—from payouts to refunds to loyalty. We’ll also show how Ansa helps marketplaces streamline payments, lower transaction costs, and unlock new ways to drive retention with stored value wallets and incentives.

From your local farmer to the largest retail platforms on earth, marketplaces are increasingly the way consumers find the goods they want, and merchants find the consumers they need. Let’s take a minute to talk about the types of marketplaces this blog will be useful for:

Have an additional use case in mind? We love to solution with folks! Just share your information in this form and one of our specialists will reach out.

So, how does it work? When a purchase is made, the marketplace sends the details of that purchase to the Ansa platform via API. Ansa decreases the buyer’s balance, increases the seller’s balance, and sets aside the marketplace’s share—all in a single API call. These flows can happen synchronously, or after your risk team clears the transaction.

Your customers only see their spendable balance, but under the hood, a lot is happening: funding sources, incentive rules, and settlement logic all drive that simple wallet balance.

Additionally, we've built in the flexibility to work with your system.

Whether you’re building a peer-to-peer community, scaling a B2B platform, or selling digital goods, the way money moves on your marketplace has a direct impact on growth. With Ansa, you can simplify complex payment flows, reduce costs, and turn transactions into opportunities to keep buyers and sellers engaged.

If you’re ready to explore how a stored value wallet and incentive engine can work for your marketplace, our team would love to show you what’s possible.

%20Large.jpeg)

.webp)

.png)